|

|

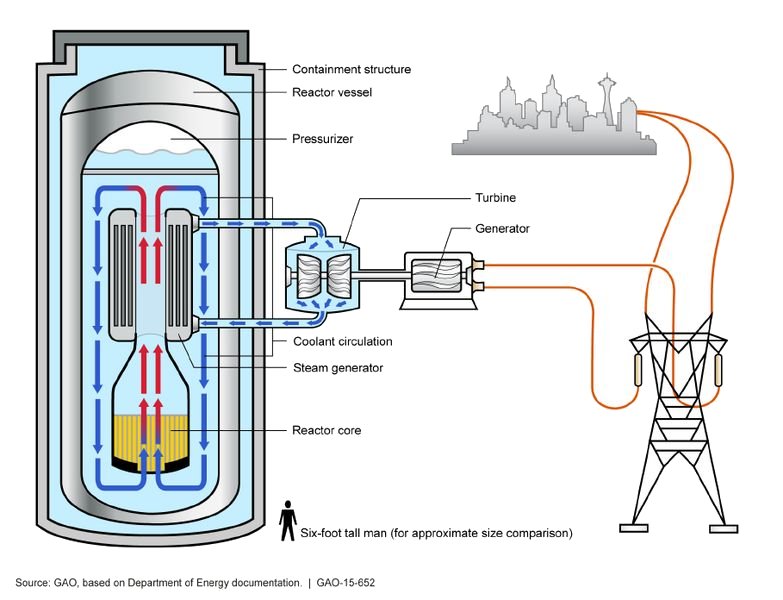

| Fig. 1: Illustration of a basic Small Modular Reactor (SMR). [6] (Courtesy of the GAO) |

On August 15, 2011, the CEO of Exelon Energy John Rowe presented a scathing review of the economics of new nuclear in a presentation titled "My Last Nuclear Speech." This came as a shock, leading many to bemoan the "death of nuclear energy". If anyone was to herald good news about the future of nuclear, it should be Rowe: Exelon's portfolio was composed of 93% nuclear at the time. However, as he somewhat infamously explained, nuclear "is a business, not a religion," and with lower natural gas prices, investment in nuclear was simply uneconomic. Today, Exelon is still a leader in clean energy, with a nuclear arm that operates America's largest fleet of nuclear plants at a 93.7% capacity factor. But the composition of their portfolio has changed drastically: Exelon Power has seen huge investments, with 20% of the Exelon portfolio now invested in natural gas, while Exelon Nuclear now manages only 64% of Exelon's generating capacity. In many ways, Rowe's prediction in 2011 that "the business of new nuclear will be miserably hard and extremely challenged by economics" seems to be accurate.

Given Rowe's comments, many questioned why Exelon hadn't immediately sold off its existing nuclear plants and invested in gas-fired generation; however, these people missed the point or Rowe's speech almost entirely. Rowe was not bemoaning the efficiency of nuclear plants once established: the operation costs (measured using levelized cost) of nuclear plants comprise about 10% of total electricity cost, compared to about 70% for natural gas. However, capital costs (especially the cost of premiums paid to investors) comprise about 80% of a nuclear plant's total electricity cost. [1] Thus, while established nuclear is a winning investment, the front-loaded costs of new nuclear make it a prohibitively difficult proposition. While this can be abated in a regulated market (CWIP financing allows a utility to collect some of the financing costs up front, lowering the total amount financed), new nuclear in deregulated energy markets is extremely risky. Natural gas does not face this handicap but introduces significantly more uncertainty, as future energy prices are heavily tied to the future cost of gas.

While Rowe was optimistic about the future of established nuclear, recent events have suggested that deregulation can adversely affect even these plants under the right circumstances. In their examination of the 2012 exit decision of the San Onofre Nuclear Generating Station (SONGS) plant in California, Lucas Davis and Catherine Hausman found that the closure:

Increased the private cost of electricity generation by $350 million during the first twelve months. By comparison, the annual fixed costs of keeping the plant open were around $340 million, supporting Rowe's (and others') anecdotal reports about power plant profitability. $40 million of these costs were not predicted by the pre-period supply curve, reflecting serious transmission constraints and other physical limitations of the grid. These constraints had a number of effects, perhaps most amazingly creating a noncompetitive environment for at least one company according to the paper's findings.

Had serious negative environmental impacts. The large majority of the generating capacity lost with the closure of the plant was replaced by natural gas production, which increased the carbon dioxide emissions by 9 million metric tons in the first twelve months. At the US government set rate of $37 per ton, this would constitute $333 million in additional losses in the first twelve months (and likely every year afterwards). [2]

While the Davis and Hausman articles ends on a positive note, there is no denying that the effect of low cost Natural Gas could accelerate the decline in established nuclear despite massive social and economic costs. Exelon has experienced similar problems in recent years, even appearing before Senate Energy and Public Utilities Commission of Illinois in 2015 to plead for a Zero Emission Standard. While this is no doubt motivated to some extent by Exelon's profit line, it should not be ignored. As Tim Hanley, Senior Vice President of Nuclear Projects for Exelon Generation, said in the hearing "Unfortunately, the plants aren't like cars, which can be turned off and on with the turn of a key. They are extremely complex and sophisticated machines. Once they're shut down, there's no turning back. The value of the plants will be forever lost." [3]

It seems obvious that nuclear energy has a cost problem in deregulated markets. While plants that are well-established (and not near retirement) can operate at costs lower than natural gas plants, the capital costs of setting up a nuclear plant are prohibitive. However, most agree the long-term environmental (and economic) costs of using solely natural gas are prohibitive, leading us to ask the question: what gives? In this battle between sustainability and scalability, who wins? While the shift towards natural gas is irrational when viewed in the right way, there is a common saying for investors wishing to bet against irrationality in the market that goes something like this: "The market can remain irrational longer than you can remain solvent." In other words, while it may be irrational to continue to invest in a form of energy that is more expensive in the long-term, energy companies have to practically behave according to market forces.

However, there is hope for nuclear energy. While the large scale nuclear plants of the past may not be immediately scalable in deregulated markets, small modular reactors (SMRs, see Fig. 1) are being produced to allow companies to invest in nuclear without "betting the farm" on every plant. These reactors are small enough (see image above to compare against average human) that they can be built in factories and do not require nearly the same level of capitalization as traditional plants due to their size (lower cost of construction and smaller plots of land). They use molten salt as a coolant (allowing for a plant that is "walk-away safe") and can generate electricity at roughly half the cost (per megawatt) of larger facilities. As with any power source, these have their fare share of barriers. They are limited to extremely small generation levels (traditionally about 200 megawatts) relative to their traditional counterparts (1000+ megawatts) and the Nuclear Regulatory Commission's certification process currently focuses on light-water reactors. [4] However, with the number of companies increasing every year, this economy of scale should adjust nicely over the coming years. After all, many companies are left with no choice. Nuclear energy as traditionally imagined will not survive, and deregulated energy markets have no interest in bailing out utilities. [5]

© Jim Grace. The author grants permission to copy, distribute and display this work in unaltered form, with attribution to the author, for noncommercial purposes only. All other rights, including commercial rights, are reserved to the author.

[1] "Annual Energy Outlook 2017," U.S. Energy Information Administration, 5 Jan 2017.

[2] L. Davis and C. Hausman, "Market Impacts of a Nuclear Power Plant Closure," Am. Econ. J. - Appl. Econ. 8, No. 2, 92 (April 2016).

[3] D. Fein and T. Hanley, "Next Generation Energy Plan: Testimony to the Senate Energy and Public Utilities Committee," Exelon Corp, 19 May 15.

[4] K. Bullis, "Safer Nuclear Power, at Half the Price," Technology Review, 12 Mar 13.

[5] R. Smith, "Nuclear Power Goes Begging, Likely at Consumers' Expense," Wall Street Journal, 17 Apr 15.

[6] "Nuclear Reactors: Status and Challenges in Development and Deployment of New Commercial Concepts," U.S. General Accounting Office, GAO-15-562, July 2015.