|

|

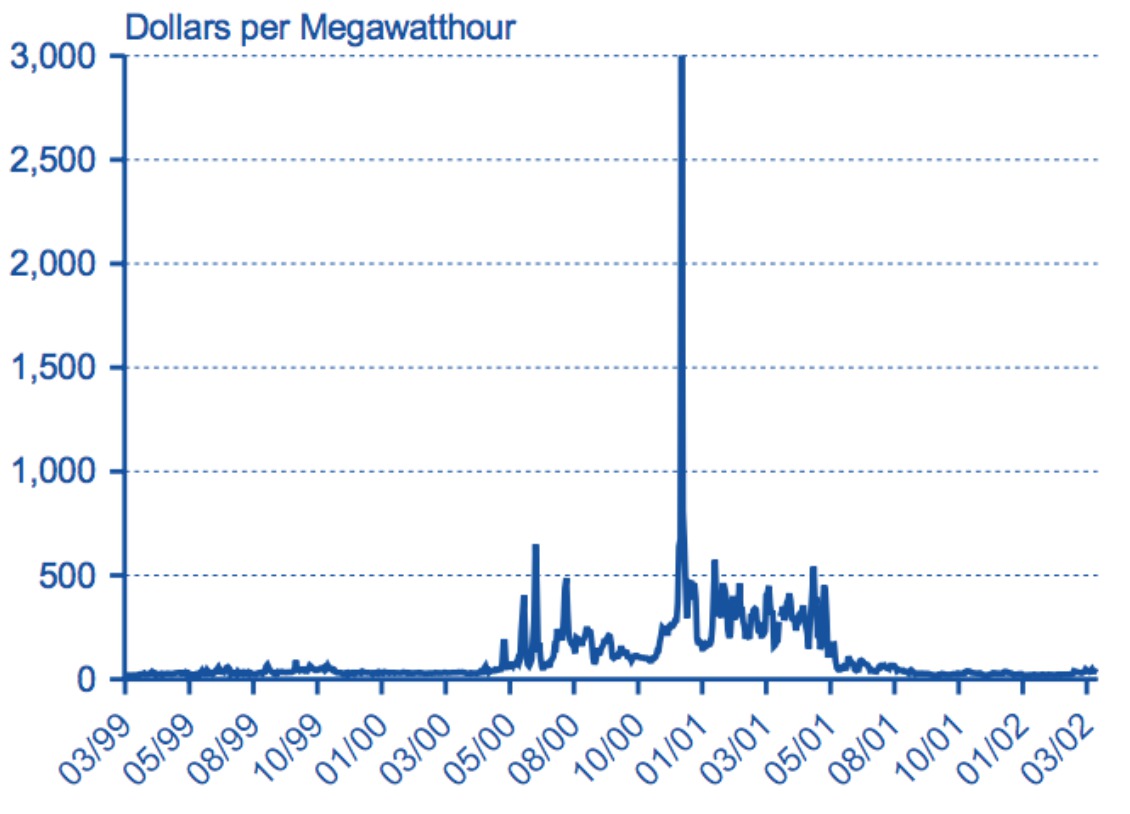

| Fig. 1: Spot price per MWh of electricity at the California-Oregon border from 1999 to 2002. [1] (Courtesy of the EIA) |

Derivative securities are financial instruments whose value is derived from that of some underlying good, for instance the value of a capital stock or a barrel of oil. The fundamental purpose of derivatives in any market is to transfer risk. They can be used by a farmer to lock in the selling price of corn three months from now, by an airline to lock in the price of fuel for flights throughout the next year, and even by a ski resort to hedge against the risk of a warm winter. [1] On the other side of all of these transactions is a "speculator" who takes on the risk with the hope of making a profit. The usefulness of derivatives in the energy market, to both the hedger and the speculator, has made them very popular in recent years. In fact, the amount of crude oil represented by derivative contracts now greatly exceeds the actual global demand for physical oil. [2] This page will provide an overview of the structure, function, and impact of these derivative securities in the energy market.

There are a large variety of derivatives available on the market but the most common are forwards, futures, and options. Forward contracts represent an obligation between two parties to buy/sell a certain quantity of a good at a specific, future date. Futures are structured in the same fashion as forwards except that they trade on organized, open exchanges and follow standardized contract specifications. Since futures trade on open exchanges, there is much more price transparency relative to forwards and the prices are more reflective of the market consensus for the contract value. They are therefore important trackers of the expected value of the underlying good at the contract settlement date as well as the interim market volatility. Options can be structured in many different ways but in general they are similar in form to futures contracts except that instead of an obligation between two parties to buy/sell, one party pays a premium for the option to do so. [3]

All of these derivatives are contracts between two parties, one who takes a "long" position, profiting if the value of the asset increases, and one who takes a "short" position, profiting if the asset value falls. Apart from intermediary fees, this is a zero sum game. What one party loses, the other party gains.

In theory, energy derivatives can be extremely useful to entities wishing to reduce their exposure to the risk of market fluctuations. This exposure can often be fatal to corporations which do not have sufficient liquid capital to sustain themselves during surges. For instance, in 1998 wholesale power prices in US Midwest skyrocketed from $30-$60 per MWh to $7000 per MWh which caused the bankruptcy of two power marketers on the east coast because they did not adequately hedge against this risk. [3] Additionally, the California energy crisis of 2000/2001 could have been avoided entirely if utility providers reduced their exposure to the the volatile spot market price shown in Fig. 1. [3]

Forwards, futures, and options allow corporations to protect against such price surges by locking in their future energy costs. In principle, this security can then be transferred to the customer who, for example, may see reasonable stability in the prices of flights even when the spot price of fuel is volatile. Derivatives also provide a great deal of security on the wholesale supply side of the energy market. For instance, extracting oil from the Canadian oil sands is a relatively costly process and is only profitable if the supply price of oil remains above some threshold. Given the volatility of the oil market, it would be extremely risky to make the heavy capital investments necessary to begin extraction. However, effective use of derivative contracts can lock in the supply price for the next several years and guarantee profitability of the endeavour even in the face of market uncertainty.

Clearly energy derivatives fill a valuable niche by providing a means for sellers to lock in future sales prices and buyers to lock in the cost of their future energy requirements. If these contracts were made directly between energy providers and consumers, the sole activity would be two parties hedging their risk against market uncertainties. In practice, derivative contracts are rarely held from purchase to maturity (the point at which the underlying energy would be delivered at the price specified in the future/option). Instead, the market is filled with speculators who have absolutely no interest in receiving the underlying good, be it barrels of oil or MWh of energy. Speculators attempt to model future economic, political, and environmental conditions in order to determine the future price of these derivatives. They then make plays in the derivative market in an attempt to profit off of their "superior" knowledge. For example, this can be done by purchasing futures/options on the open exchange and selling them at a higher price (prior to maturity) for a profit. These transactions are typically done on margin, meaning that the speculators use large amounts of debt to finance their purchases, amplifying the impact of any gains or losses in the asset value. [1]

Let's consider a large group of speculators who have taken short positions in the crude oil market. This means that the speculators are expecting the price of crude oil to decrease in the future and if the price does decrease, they can close their positions for profit. These positions are heavily leveraged and have the potential for unlimited losses/gains at the cost of extreme sensitivity to price fluctuations. If the price of oil now starts to increase, speculators will begin to close their positions in an attempt to cut their losses. This causes the price of oil to rise even further resulting in more short positions to be closed which further drives up the price and so on. This vicious positive reinforcement phenomenon is termed a "short squeeze" and is widely believed to be responsible for the oil bubble in 2008. [4] The result is that a massive increase in the price of crude oil is observed even though the fundamental change in supply and demand that caused the initial price increase may have been minimal. It is through such actions that speculators can have a tremendous impact on the price of real goods without ever actually purchasing or selling the physical asset.

In theory, energy derivatives provide a valuable tool for the hedging of risk. However, the invention of more and more complicated derivative instruments combined with a large population of speculators may be exposing the price of the physical, underlying good to increased volatility. The jury is still out on this however, as many arguements have been put forth to support the idea that derivatives have no substantial impact on the volatility of the energy market. [5,6] Nevertheless, speculators do play a valuable role in the derivative market; namely, they provide liquidity in the market so that derivatives can be readily purchased by interested parties. Furthermore, speculators actively incorporate information about the evolution of the global energy market into the price of derivatives, increasing the efficiency of the market. [2] The question remains as to whether energy derivatives should be further regulated so as to minimize any potential harmful effects that speculation and associated feedback cycles could have on the energy market.

© Emil Noordeh. The author warrants that the work is the author's own and that Stanford University provided no input other than typesetting and referencing guidelines. The author grants permission to copy, distribute and display this work in unaltered form, with attribution to the author, for noncommercial purposes only. All other rights, including commercial rights, are reserved to the author.

[1] "Derivatives and Risk Management in the Petroleum, Natural Gas, and Electricity Industries," US Energy Information Administration, October 2002.

[2] D. Berryrieser, "Crude Oil Futures," Physics 240, Stanford University, Fall 2011.

[3] S. J. Deng and S. S. Oren, "Electricity Derivatives and Risk Management," Energy 31, 940 (2006).

[4] D. Tokic, "Rational Destabilizing Speculation, Positive Feedback Trading, and the Oil Bubble of 2008," Energy Policy 39, 2051 (2011).

[5] P. Krugman, "The Oil Nonbubble," New York Times, 12 May 08.

[6] J. Fleming and B. Ostdiek, "The Impact of Energy Derivatives on the Crude Oil Market," Energy Econ. 21, 135 (1999).