|

|

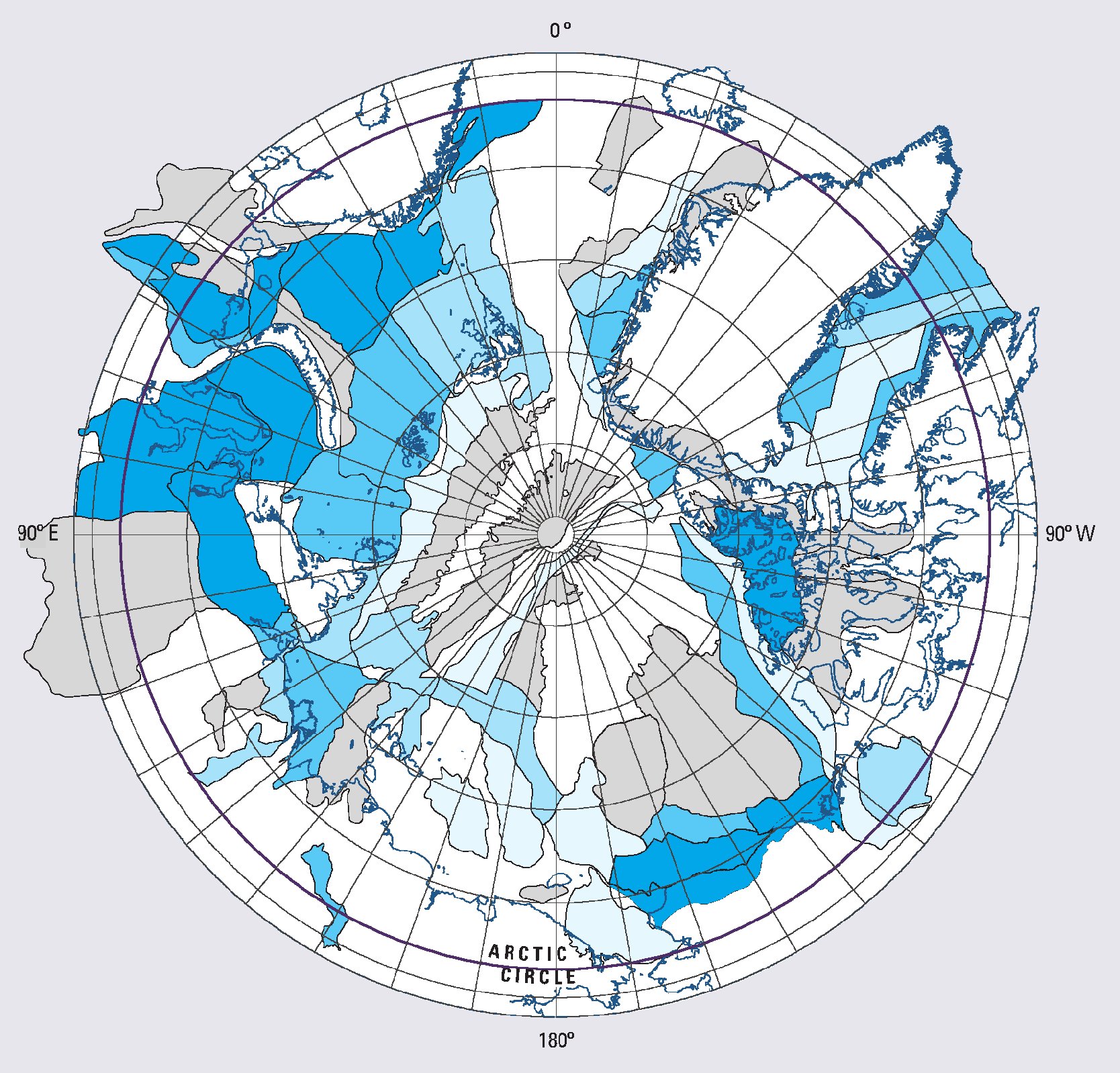

| Fig. 1: Probability of the presence of undiscovered oil/gas fields with significant amount of recoverable resources (> 50 million barrels of oil equivalent).across various regions in the Arctic. A stonger hue of blue means a higher probability. [5] (Courtesy of the USGS) |

When thinking about oil production, one tends to imagine countries of the Middle East or the Mexican gulf, but only rarely the regions beyond the Arctic circle (latitude 66.55° north of the equator). However, the public awareness of the arctic oil and natural gas reserves seems to be increasing. Shell's recent drilling activities in the Chukchi and Beaufort seas, and their recent abandonment of the area, may have been the most important trigger for this. [1,2] The discussion following Shell's decision to stop drilling in the arctic (see Barrett for example) contains virtually all the elements that pertain to the issue: [3]

Financial interests of both the drilling companies and those of the regulatory bodies - the challenging climatic conditions in the North require non-standard (and expensive) precautions to be taken. Furthermore, as of now, the infrastructure for the efficient transport of the extracted commodities is lacking.

Environmental considerations - drilling for oil and natural gas are both activities with potentially large environmental impact. Many organizations expressed concern about drilling activities influencing, or even destroying, the fragile ecosystems in the Arctic.

Politics - which could be said to connect the two previous items. Drilling for the natural resources is a heavily regulated industry and as such prone to be influenced by the politics.

The attractiveness of the arctic regions to the governments stems from the large estimated quantities of undiscovered oil and gas (illustrated in the map in Fig. 1, where the strength of the hue of blue means the probability of significant undiscovered resources present in a given geographical region) and the potential lowering of the energetic dependence of a given country on the imports. Global climate change that is shrinking the ice coverage of the Arctic ocean from year to year, removes many engineering and logistic obstacles present in the past.

There are six countries with regions beyond the Arctic circle and with direct access to the Arctic ocean - Russia, USA, Canada, Norway, Denmark (via Greenland) and Iceland. At the present only the first four countries listed are actively drilling for oil an natural gas in these areas. [4]

Currently the latest estimate of the conventional oil and gas reserves beyond the Arctic circle has been carried out by the U.S. Geological Survey (USGS) in 2008. [5] At the time of its writing, the existing fields beyond the Arctic circle contained about 240 billion proven barrels of oil and oil-equivalent natural gas (this includes both production and remaining resources), comprising about 10% of the world's existing conventional resources. The amount of undiscovered resources is calculated without considering economical or other factors, such as the convenience or the economical viability of drilling. As such, the Arctic is estimated to contain about 90 billion barrels of undiscovered oil, 17 trillion cubic feet of undiscovered gas and 44 billion barrels of natural gas liquids, making up, respectively, 16%, 30% and 26% of the world's individual undiscovered hydrocarbon resources. [6] Roughly 84% of the undiscovered Arctic resources are expected to be found offshore.

With a relatively high abundance of hydrocarbon supplies, the Arctic sounds like a good candidate for the expansion of the oil industry. However, severe obstacles exist that hamper this effort by increasing the cost of this expansion significantly. In this section we discuss these issues in detail.

The specific challenges encountered in the extreme - and, recently, changing - climate beyond the Arctic circle have been discussed by. [5] Slowly receding ice cover of the Arctic ocean works both in favour and against the drilling efforts. Shipping of the mined resources via traditional naval routes becomes easier, as they remain ice-free for longer time periods during the summer season. On the other hand, no current model predicts a completely ice-free winters in the Arctic ocean, as opposed to the fields further south. This puts constraints both on the shipping of the resources (since the current takers cannot navigate through ice fields) but, more importantly, on the design of the drilling platforms, that, if designed improperly, could be easily damaged by a collision with an ice berg. On land, the transport gets complicated in summer, when the top layer of the permafrost melts into mud unable to support heavy machinery required for the job.

With the shrinking ice cover, the weather patterns are expected to change as well and instability is introduced into what used to be a relatively predictable system. Harsh weather conditions mean more costs. Additionally, with the reduced ice cover, the force of waves on the ocean is expected to rise, increasing the danger of the transport.

Fragile but harsh Arctic environment requires special disaster-prevention measures to be in place. This became especially clear after the Deepwater Horizon spill in the Mexican gulf in 2010. A disaster on such scale would be especially devastating in the Arctic, where the oil would not be able to evaporate from the water (as was the case for an estimated 25% of the oil in the Mexican gulf, that either evaporated or dissolved in the water). [7] Additionally, due to the low population density in the Nordic areas, the required manpower to handle such a disaster would be problematic, if not impossible, to accumulate.

With these issues in mind, the question of economic viability of drilling in the Arctic naturally comes up. [8] Try to answer this question by simulating the volume of oil and gas production in the Arctic from 2010 till 2050 in various model scenarios. A simplifying assumption is made, where the system is defined with a completely free market with no political obstacles and environmental concerns. In order to estimate their uncertainties, in their reference scenario they assume the evolution of prices from the literature (peaking at $115 per barrel in 2030, assuming 2008 dollars) and compare this with a "High price" scenario when the price of oil steadily rises, peaking at $140 (2008 dollars) per barrel and remaining constant, and a low-resource scenario, in which only half of the undiscovered resources (from Gautier et al.) turn out real. [5] They conclude that even though almost a quarter of the world's undiscovered hydrocarbon supplies are situated in the Arctic, in the future no more than 10% of the world's production is expected to come from here, as cheaper alternatives from the Middle East, as well as unconventional resources, will dominate.

In the previous sections we covered the physical amount of hydrocarbon resources in the Arctic, natural factors influencing its availability and finally the economy of the drilling. This section discusses the last part of the story - with the oil and natural gas' crucial importance to the society, the decisions about potential drilling activities beyond the Arctic circle are deeply influenced by the politics. The countries with direct access to the Arctic ocean have diverse political statuses and policies and we talk about each of them individually.

Iceland is the newest player in the game, having decided to start granting exploration drilling licences only recently. A first call for applications in 2009 ended unsuccessfully, as both competitors withdrew their applications eventually. In a more recent call, from 2012, the first two licences have been awarded for exploring regions around the Jan Mayen ridge, lying to the north of Iceland. [9] At the time of writing of this report, there do not seem to be any more recent developments concerning the oil drilling in Iceland.

The drilling philosophy of Norway is driven by two opposite influences. As a strong supporter of the Kyoto agreement, the country pursues reducing the CO2 emissions and furthermore, off-shore drilling gets into conflict with the local fishing industry. On the other hand stands the fact, that oil and gas related activities contribute more than one fifth of Norway's GDP and hydrocarbon resources are its main export constituents. [10] Coming to the ongoing activities, in 2007, Norway started the first liquefied natural gas (LNG) project in Europe on the Snohvit field (140km off-shore from a northern town of Hammerfest), providing 6bn cubic meters of gas annually. [11] A resulting development of the infrastructure in the area resulted in 2009 in approval of the plans for development of the nearby Goliat field. As of earlier this year (2015), a new oil rig was on its way to the field, despite the cost of oil production ($95 per barrel) being below the oil prices at the market ($75). [12] Finally, suggesting that GDP is a priority over the environment, additional 20 licences for exploration and development were awarded in 2013. [13]

Russia has been a famously problematic country for the international investors, who, attracted by its vast natural resources, have often encountered legislative obstacles such as being forbidden to export the resources themselves, which is by law only allowed to the state-owned monopolies, Gazprom and Rosneft. [13] Russia lacks coherent strategy when it comes to hydrocarbons. Even though they signed the Kyoto agreement, local authorities do not seem to worry about the environment too much and do not pursue the development of alternative energy sources. [4]

Currently, Russia is pursuing a new on-shore gas project on the Yamal peninsula, that should provide gas for Europe via pipeline and also LNG (16.5 million tons annually) produced on-site and transported to the markets in the northeastern Asia via a fleet of special ice-breaking ships. Two important off-shore fields deserve a mention. Plans for development in the Prirazlomnoye field, lying in a shallow (20m) sea about 57km from the mainland in the Barents sea, have been discussed since the 1990s, however the production only started in December 2013 at the level of 6.5 million tons of oil a year, making it the first offshore oil project in the Arctic. The unique feature of this project is its drilling platform, made of concrete and sitting on the seabed, which, as the first of its kind, has been designed to withstand collisions with ice. The Shtokman gas field, where the test drills found a supply estimated 3.8 trillion cubic meters, could have become the biggest discovered gas field in the world. However, the project has been shelved after more than two decades (discovery in 1988 and shelving in 2012) of political struggle. [13] Originally offered for the development to foreign investors, the plans were later scrapped as Gazprom decided to develop the field on its own. Between 2003 and 2008, when the market for the LNG seemed attractive, the plans for development were continued and eventually, an company involving international know-how, Shtokman AG, was set up. However, plagued by technical disagreements, no activity started till 2012, when the market changed to make the project unprofitable at the time being, with no current plans for a resurrection. Finally, the majority of the future plans of offshore oil drilling in Russia were halted, or at least hampered, by the western sanctions. [14]

Forty percent of the area of Canada lies north of the Arctic circle which contains significant oil and natural gas resources. Although pointing out their concern for the environment and the importance of protecting the life style of the natives, the activities regarding oil and gas in the Canadian north were supported by the previous conservative government. A detailed report on the activities and available resources has been published by the Oslo-based Arctic Monitoring and Assessment Program, who report on complicated structure of responsibility for the natural resources that differs among the individual provinces and is divided between the federal and local governments. [15] As a traditional exporter of oil and gas, the production of Canada depends on the international demand (for example, 7% of oil and 16% of natural gas of the USA has been provided by Canada by the end of 2003). [15] A long term subject of negotiations has been the Mackenzie Gas Project, a construction of 1200km long gas pipeline connecting potential natural gas producing facilities in the Mackenzie river delta with markets further south in Alberta. After the initial stalling due to the development of unconventional gas on the international markets, the project got support from the government in 2013, with the possibility of export to the Asian markets. [16] However, after a recent increase in the projected cost, the final decision on building has been postponed due to the natural gas market conditions. [17] Canadian new government has not, at the time of writing, made any decisions on the arctic oil issues beyond general pre-election promises.

In the USA, the future drilling activities have been influenced by the 2010 Deepwater Horizon oil spill and new drilling licences have been awarded reluctantly and with an eye on public opinion, especially in the problematic and fragile Arctic environment. More importantly, even though currently about 13% of the oil production in the USA comes from beyond the Arctic circle, with the development of unconventional gas and oil drilling, further development in the harsh (and expensive) Nordic conditions is not crucial at the moment. [15] Recently, awarding new leases for drilling in the Arctic has been curbed by the US government. [18]

The unique features of the political situation of Greenland stem from its status of an autonomous country under the Danish crown. As such, its government has authority over its natural resources, however, Denmark remains responsible over its foreign policies, including signing off any contracts with foreign companies seeking to explore the presence of natural resources and their excavation. Due to the high potential for a disaster discussed in the previous section, the government of Greenland asks an for an upfront payment of $2 billion from the companies willing to drill to be able to efficiently deal with a spill. [19] After a minor halt in handing out the drilling licences in 2013, British Petroleum (BP) won the first drilling concession in 2014 in a relatively surprising decision, given the company's past responsibility for the Deepwater Horizon spill. [20,21]

The future of oil and gas drilling in the Arctic is a problem with many uncertainties. Even though with a high degree of certainty it contains a large amount of natural resources, their actual recovery depends on many hard-to-predict factors from the climate change and the development of the world's economy to the political situation in the individual countries with the access to the resources.

© Ondrej Urban. The author grants permission to copy, distribute and display this work in unaltered form, with attribution to the author, for noncommercial purposes only. All other rights, including commercial rights, are reserved to the author.

[1] Y. Rosen, "Shell Finishes Arctic Drilling For Season, Plans More in 2013," Reuters, 31 Oct 12.

[2] T. Mcalister, "Shell Abandons Alaska Arctic Drilling," The Guardian, 28 Sep 15.

[3] P. Barrett, "Why Shell Quit Drilling in the Arctic," Bloomberg Business, 29 Sep 15.

[4] Ø. Harsem, A. Eide, and K. Heen, "Factors Influencing Future Oil and Gas Prospects in the Arctic," Energy Policy 39, 8047 (2011).

[5] D. L. Gautier et al., "Circum-Arctic Resource Appraisal: Estimates of Undiscovered Oil and Gas North of the Arctic Circle," U.S. Geological Survey, USGS Fact Sheet 2008-3049, 2008.

[6] M. E. Brownfield et al., "An Estimate of Undiscovered Conventional Oil and Gas Resources of the World," U.S. Geological Survey, USGS Fact Sheet 2012-3024, 2012.

[7] R. A. Kerr, "A Lot of Oil on the Loose, Not So Much to Be Found," Science 329, 734 (2010).

[8] L. Lindholt and S. Glomsrød, "The Arctic: No Big Bonanza for the Global Petroleum Industry," Energy Econ. 34, 1465 (2012).

[9] B. Gardiner, "Iceland Aims to Seize Opportunities in Oil Exploration," New York Times, 1 Oct 13.

[10] T. Dorsey et al., "Norway: Selected Issues," International Monetary Fund, IMF Country Report No. 15/250, September 2015.

[11] A. Moe, "Russian and Norwegian Strategies in the Barents Sea," Arct. Rev. Law Polit. 1, 225 (2010).

[12] J. K. Bourne, "This Giant Oil Rig Could Usher in a Radically Altered Arctic," National Geographic, 23 Apr 15.

[13] A. Moe, "Russian and Norwegian Perspectives," in The Arctic in World Affairs, ed. by O. R. Young, J. D. Kim, Y. H. Kim, Korean Maritime Institute, December 2013, p. 169.

[14] E. Mazneva, "Sanctions, Oil Slump Delay Russian Offshore Drilling 2-3 Years, Bloomberg Business, 29 Sep 15.

[15] "Assessment 2007: Oil and Gas Activities in the Arctic - Effects and Potential Effects. Volume I," Arctic Monitoring and Assessment Programme (AMAP), 2010, Ch. 2

[16] M. McDiarmid, "Mackenzie Valley Pipeline Facing Possible Revival," CBC News, 25 Oct 13.

[17] "Cost of Imperial's Mackenzie Gas Project Hits More Than C$20 Bln.," Reuters, 24 Dec 13.

[18] A. Harder, U.S. Cancels Sale of Two Arctic Oil and Gas Leases," Wall Street Journal, 16 Oct 15.

[19] T. Webb, "Greenland Wants $2Bn Bond From Oil Firms Keen to Drill in Its Arctic Waters," The Guardian, 11 Nov 10.

[20] T. Mcalister, "Greenland Halts New Oil Drilling Licenses," The Guardian, 27 Mar 13.

[21] T. Mcalister, "BP Wins First Greenland Drilling Concession Despite Chequered Record," The Guardian, 3 Jan 14.