|

|

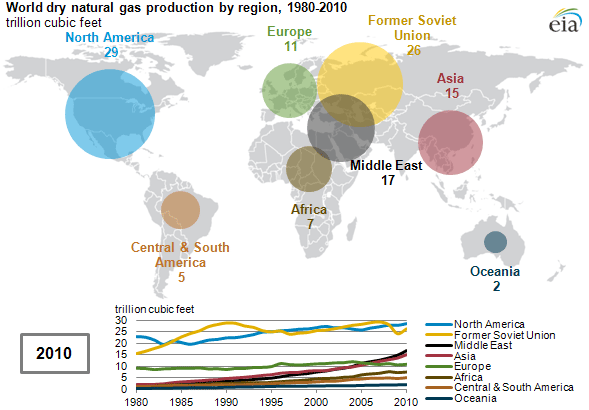

| Fig. 1: Relative worldwide natural gas production in 2010. (Courtesy of the U.S. Department of Energy) |

The natural gas industry has experienced a significant renaissance over the past decade and is destined for significant further upheaval in the coming years. Historically there have generally been three dominant natural gas markets: the United States, Europe, and Asia (mostly Japan and Korea). To date these markets have been largely isolated from each other, with US gas coming from Canada, European gas originating in Russia and Africa, and Asian gas being supplied by the Middle East. [1] However as the gas industry grows, these markets will be unable to maintain their isolation and they will integrate as natural gas becomes more of a globally traded commodity. [2]

Macro trends seem readily straightforward that global production and reserves of natural gas will continue to increase going forward, particularly with the spread of horizontal drilling and hydraulic fracturing. At the same time, huge demand increases are being driven by energy-hungry emerging markets. Furthermore, raised awareness of carbon emissions has encouraged a shift away from traditionally dirtier fossil fuels such as coal, and natural gas has been championed as a viable "clean" substitute. [3] Therefore, with huge growth anticipated both on the production side and the demand side, we can assuredly expect increased natural gas trade volume in the coming decade. How exactly this trading increase will evolve is impossible to say for certain, however an analysis of some of the most influential projects currently in development will help understand likely future scenarios. The following five projects are poised to fundamentally disrupt the natural gas landscape.

Russia's natural gas exports have historically been focused almost exclusively on Europe. The Eastern Gas Program, one of the biggest projects being pursued by Gazprom, is intended to develop the gas sector in eastern Russia. The program consists of a collection of infrastructure projects including various gas production centers, hundreds of miles of pipeline, and further development of LNG terminals on Russia's eastern coast. It is estimated that by 2030 the Eastern Gas Program will add up to 7 trillion cubic meters of natural gas to the existing resource base in the Siberian and Far Eastern Federal Districts.

Particularly noteworthy about the project is the prospect to install pipelines from Russia to Korea or China. This would be a dramatic shift in global gas markets as Russia would then serve as a direct bridge between the European and Asian markets. It represents a long-term Russian investment in Asian natural gas demand and it will give Russia significantly increased flexibility to allocate gas resources globally for maximum economic gain. The implications of the Eastern Gas Program are far-reaching as it will be an institutionalized break in the regionally isolated gas markets. Asia will be able to source gas from the Middle East or from Russia, leading to price competition that will compress price spreads globally.

Ever since 15 European countries were affected by natural gas shortages or outages in 2009 as the result of a dispute between Ukraine and Russia, the European Union has made it a priority to diversify energy sources. Currently Europe obtains almost half of its natural gas through Russian pipelines with most of the rest being produced internally or shipped as LNG from Qatar. The Southern Gas Corridor is a vaguely defined initiative to build pipeline directly linking Europe to Caspian and Central Asian gas supplies, bypassing Russia. This would give European nations a stable secondary supply that diversifies both the source and the route, effectively breaking Russia's monopoly on Europe. [4]

Naturally Russia and Gazprom are generally opposed to this project and so Gazprom has proposed a competitor project called South Stream that will also pipe gas into southern Europe, though this would still be Russian gas. The pipeline would run under the Black Sea, originating in Russkaya, and come ashore in Bulgaria. Gazprom promotes this project as offering diversification of route, as this pipeline would avoid Ukraine and so would not be threatened by Russia/Ukraine disputes. The South Stream project is scheduled to begin construction before the end of 2012. The EU states that it remains committed to the Southern Gas Corridor to gain access to Turkish and Azeri gas, but the project is still early in development. It remains to be seen whether the Southern Gas Corridor will proceed regardless of installation of the South Stream.

This interaction especially highlights some of the tradeoffs between natural gas trade via pipeline and LNG. The coming years will likely see a global shift away from pipelines, with investment instead going to LNG. The geopolitical risks associated with international pipelines are proving too great given the generally critical nature of gas imports. Further, LNG affords a level of flexibility in source and route, which will be advantageous in globally integrating gas markets.

The next area that undeniably deserves attention is Australia, which is investing roughly $180 billion in developing its LNG infrastructure. There are currently at least 10 new projects scheduled for the next eight years and it is estimated that by 2017 Australia could be at more than 10 billion cubic feet per day capacity, overtaking Qatar as the world's leading LNG producer. The logical target market for Australia's gas is Asia, with China and India expected to experience steady increase in demand, but with a robust LNG industry, Australia could take advantage of markets globally. [3,5]

The attractive emerging economies in Asia have not gone unnoticed by other natural gas entrants, and East Africa promises to be a contender for some of this market. Over the past two years, over 100 TCF of recoverable gas reserves have been identified in Mozambique and Tanzania, and this number could potentially double. To date all African LNG has been centered around Nigeria and Algeria, so this is a major development to shift attention east on the continent.

Naturally it will take a long time to develop these newly discovered reserves, but already discussions have shifted from exploration and appraisal to LNG exports. As oil companies make investment decisions to support rising Asian energy demands, the east Africa area has the advantage of cheaper labor and material costs, however this is somewhat offset by a lack of critical infrastructure. Further, regulatory challenges in Africa could prove formidable as these nations learn how to manage the immense new resources. All that said, though, it is estimated that four processing trains could be operational by as early as 2018.

Finally, no discussion of current natural gas trends would be complete without mention of the American shale gas revolution. Advances in horizontal drilling and hydraulic fracturing have given rise to a sizable excess of gas supply, pressuring gas prices to their lowest level in years. With current forecasts natural gas supply could exceed demand by 2016, enabling North America to become a new exporter of LNG. This represents a dramatic and fundamental shift in global energy flows and further reinforces the likelihood of a globally integrated gas market. The current global price differentials are unsustainable and businesses will be seeking to take advantage of the arbitrage opportunity.

Given these five pivotal projects or regions, it is certain that the natural gas industry will be undergoing some major transformations in the coming years. While there are certainly many significant barriers yet to be overcome, we can expect infrastructure investment to try to capitalize on arbitrage opportunities, effectively shattering the previously isolated regional markets and creating an integrated global market. No longer could different pricing structures persist except insofar as they reflect transportation costs between markets.

An interesting question in this scenario, however, is whether a globally integrated market would allow conventional energy-rich countries to dominate. In many ways, the regionalization of gas markets has been what has allowed unconventional techniques to flourish in markets without convenient access to Russia or the Middle East. Once all these markets are interconnected, could Russia and the Middle East take corner the market with cheap gas that makes complex processes like fracking uneconomical? While many groups are excited about imminent US energy independence, there are studies that project the US remaining a gas importer in the scenario of a globally integrated market, simply because gas would be cheaper to import.

© Alex Pratt. The author grants permission to copy, distribute and display this work in unaltered form, with attribution to the author, for noncommercial purposes only. All other rights, including commercial rights, are reserved to the author.

[1] "BP Statistical Review of World Energy 2012," British Petroleum, June 2012.

[2] Y. Wu, "Gas Market Integration: Global Trends and Implications for the EAS Region," University of Western Australia, ERIA-DP-2011-07, November 2011.

[3] C. Flavin and S. Kitasei, "The Role of Natural Gas in a Low-Carbon Energy Economy," Worldwatch Institute, April 2010.

[4] N. Sartori, "The European Commission's Policy Towards the Southern Gas Corridor: Between National Interests and Economic Fundamentals," Istituto Affari Internazionali, January 2012.

[5] D. Jacobs, "The Global Market for Liquefied Natural Gas," Reserve Bank of Australia, September 2011), pp. 17-27.