|

|

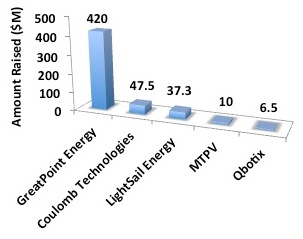

| Fig. 1: Recent cleantech venture capital deals as of 11/30/2012 (data from [5,7-9]). |

A nearly ubiquitous desire for independence from foreign energy sources, coupled with growing concerns over the environmental impact of burning fossil fuels, has driven a number of large industrialized nations -- the United States, Germany, India, and China, among others -- to focus on the development of clean energy technologies, particularly in the last decade. In the United States, technology entrepreneurship has been a major component of this groundswell, with companies like SunPower (a solar company spun out of Stanford) and A123 (a lithium-ion battery company spun out of MIT) bringing new clean technologies to market and achieving a global presence. These companies have not necessarily flourished: while one of the largest M&A deals in the last decade in cleantech was a 60% acquisition of SunPower by Total S.A. (a French oil and gas company) in 2011 for $1.3B, A123 filed for Chapter 11 recently. [1,2]

The U.S. government has supported the cleantech industry with a variety of subsidies, including about $90B of energy spending built into the Recovery Act of 2009. [3] The government's support extends all the way to early-stage startup companies; ARPA-e, a program within the Department of Energy with an annual budget of approximately $250M, has been instrumental in funding a variety of nascent high-risk clean technology ventures. [3] The private sector has played an even stronger role. Venture capital (VC) firms, which invest capital in risky, early-stage companies with the hope of massive growth of a small subset of their portfolio, have invested in many early-stage cleantech startup companies, supplying them with capital, advice, connections, and operational guidance to help them develop their technologies and business models.

Entrepreneurs over the last decade have flocked to tackling problems in cleantech, developing new technologies in transportation, energy generation (solar, wind, etc.), energy storage, smart grid, water and energy conservation, and a variety of other fields. Venture capitalists have followed suit to support these entrepreneurs and attempt to participate in their success. A number of prominent venture capital firms have played a critical role in this movement, including Khosla Ventures, with heavy investments in battery technologies (e.g. Pellion, Seeo, Quantumscape), agriculture, and energy efficiency, and Kleiner Perkins Caufield & Byers, which has invested in about 60 cleantech companies [4], including deals in electric vehicles (e.g. Fisker Automotive), energy conservation (e.g. Opower), solar finance (e.g. Clean Power Finance), and devices (e.g. MiaSol©, Nest Labs) among other fields. [4] Other important VCs operating in the cleantech space include NEA, North Bridge Venture Partners, Lux Capital, Claremont Creek Ventures, CMEA, and Technology Partners. Fig. 1 shows a number of recent VC deals in the cleantech space.

Although there has been an influx of venture capital into cleantech over the past decade, returns to investors have been limited, causing some top firms like Kleiner Perkins to recently scale back their investing in the space. [4] In the first quarter of 2012, The Cleantech Group (an industry research group) estimates that $1.3B in venture financing was raised by cleantech companies in the U.S. in a total of 113 deals. [5] While this number may seem large, according to the same research group, this amount is actually a 17% decrease from the fourth quarter of 2011 and a 36% decrease from the first quarter of 2011. [5] The collapse in the summer 2011 of the Fremont solar panel manufacturer Solyndra, which lost about $1B for its private investors, was a particularly strong negative signal for investors in the cleantech space. [6] While there is certainly a sense in Silicon Valley that cleantech has lost some of its "sexyness" over the past few years, cleantech VC has by no means disappeared, as demonstrated by the 2012 numbers given above.

Another model for supporting the growth of early stage cleantech companies that complements the role of venture capital firms is startup financing from strategic investing arms of major technology corporations. Corporate partners can bring specific industry expertise, connections, and opportunities for joint development projects that can be an invaluable resource for early-stage cleantech companies. One interesting model is Siemens' "technology-to-business" (TTB) group, which works with a variety of early stage energy companies, helping to prove technology in the field while simultaneously providing dealflow for Siemens' venture arm. This simultaneous hands-on technology partnership and investing model may prove effective in testing the viability of new clean technologies early in their life-cycle, preventing the allocation of capital to businesses that are doomed to fail. Siemens Venture Capital recently invested in Qbotix, a robotics company focused on the solar panel tracking market. [7]

Early-stage cleantech ventures face myriad challenges in growing, developing their technologies, and carving out a foothold in the (often highly entrenched) markets they are targeting. While government support for cleantech projects is beneficial at this early stage in the industry's existence, it cannot be relied on forever, and the role of the venture capital community and their counterparts at corporate investing arms will continue to grow more important to the industry in the years to come as the government inevitably winds down its subsidies. With growing adoption of electric vehicles, solar power, water conservation, and energy efficiency technologies worldwide, it's inevitable that there is money to be made for risk-tolerant investors in this space; who will have the guts to make smart investment decisions and to ride out the storm is yet to be seen.

© John Melas-Kyriazi. The author grants permission to copy, distribute and display this work in unaltered form, with attribution to the author, for noncommercial purposes only. All other rights, including commercial rights, are reserved to the author.

[1] D. R. Baker, "Total SA to Buy 60% stake in SunPower," San Francisco Chronicle, 28 Apr 12.

[2] B. Vlasic and M. L. Wald, "Maker of Batteries Files for Bankruptcy," New York Times, 16 Oct 12.

[3] J. M. Broder, "After Federal Jolt, Clean Energy Seeks New Spark," New York Times, 23 Oct 12.

[4] L. Riddell, "Top VC Kleiner Curbs Its Cleantech Commitments", San Francisco Business Times, 14 Sep 12.

[5] D. Hull, "Cleantech Investment Slows But Many Backers Remain Hopeful," San Jose Mercury News, 26 Jun 12.

[6] T. Woody, "What Solyndra's Bankruptcy Means For Silicon Valley Solar Startups," Forbes, 31 Aug 11.

[7] L. Ridell, "Robots Track Sun to Juice Solar Power", San Francisco Business Times, 7 Sep 12.

[8] A. Herndon, "Thiel Invests in LightSail Compressed-Air Storage System," Bloomberg, 5 Nov 12.

[9] K. Alspach, "Mass. Tops Calif. on Cleantech Venture Capital in Q1," Boston Business Journal, 6 Apr 12.