|

|

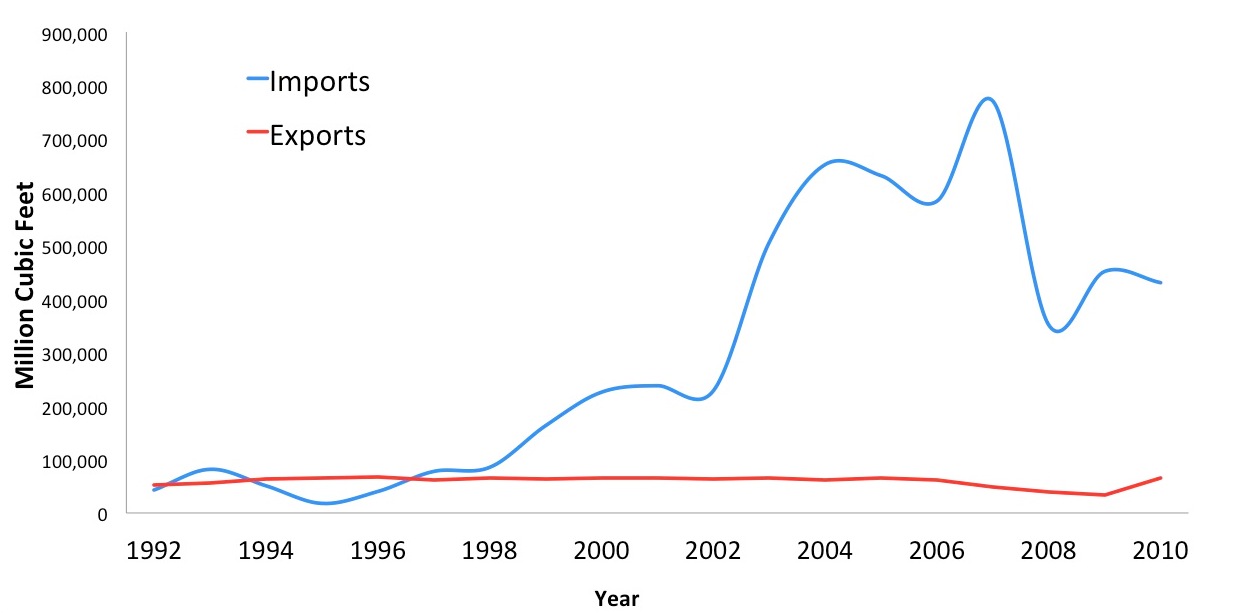

| Fig. 1: US LNG Imports and Exports, 1992-2010. [2-5] |

Liquefied natural gas (LNG), is natural gas that undergoes supercooling unit operations to a temperature of approximately negative 161 degrees Celsius at atmospheric pressure. The natural gas is therefore condensed to its liquid form and would only occupy more than 600 times less space as compared to its gaseous state. [1] In this way, it is feasible to transport natural gas over long distances in specially constructed tankers from the parts of the world where it's abundant to where it's in demand. In addition, liquefaction makes it possible to store natural gas for use during high demand periods in regions where underground storage facilities are not allowed due to unsuitable geologic conditions.

LNG possesses several merits that make it superior as compared to other energy supplies:

LNG burns more cleanly than other fossil fuels such as oil and coal since it's a basically hydrocarbon gas mixture. Upon burning, it releases fewer air emissions and leaves no ash particles, thus establishing itself as the environmentally preferred fuel of choice.

As compared to pipeline gas, LNG is purer and has higher energy content especially methane.

LNG has relatively low shipping costs over long distance, which makes it more cost efficient to transport over long distances to the parts where pipelines do not exist.

|

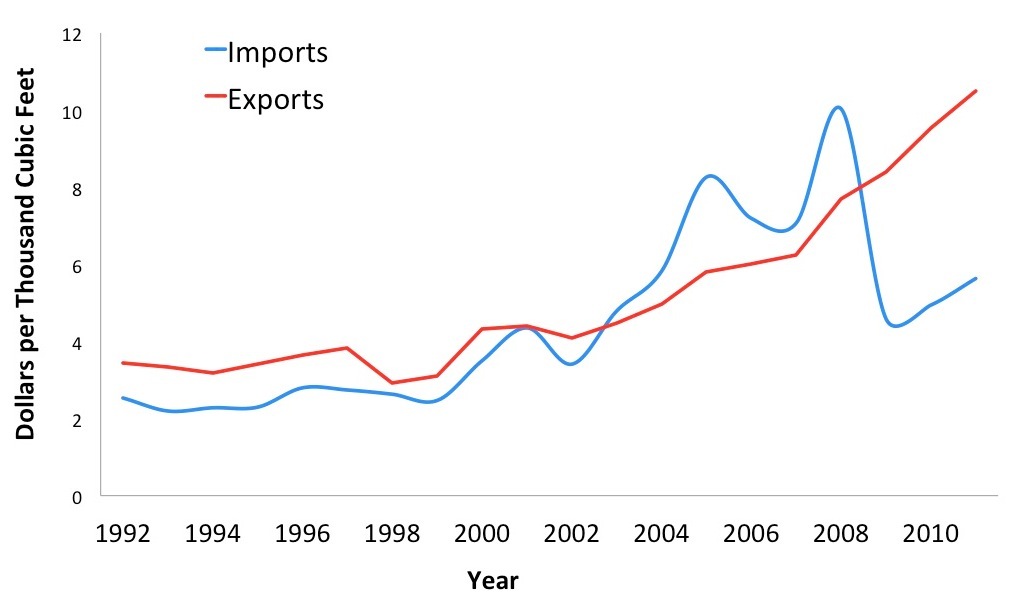

| Fig. 2: Price of US LNG Imports and Exports. [2-5] |

The plots of US LNG Imports and Exports are as shown in Fig. 1.

As seen in Fig. 1, over the decades of 1990s, the U.S. LNG imports remained at a low level. In the early 2000s, the U.S. domestic gas production declined while the demand for natural gas particularly for power generation increased, together with a dramatic rise in the U.S. natural gas prices, giving rise to the rejuvenation of the U.S. LNG market. From 2000 to 2004, LNG import almost tripled. In the later two years, the increasing trend stopped and it decreased a little. The US LNG imports experienced a sharp increase again in 2007 and then dropped dramatically by half in 2008. Although there was a small rebound in 2009, it deceased to the level as in 2008 in 2011. On the other side, the US LNG exports have kept at a relatively constant level of around 60 MMcf over the history. Exceptions happened from 2007 to 2009, during which LNG exports dropped a little. This might be due to the overall increasing trend of the export price since 21st century (Fig. 2).

The price of LNG started to skyrocket rapidly and elevate LNG price largely after year 2000 though the cost of LNG plants and tankers were reducing due to design improvements. There are several factors accounted for this speedy increase: low availability of EPC (Engineering, Procurement and Construction) contractors because of extraordinary large numbers of ongoing petroleum projects worldwide; high raw material prices; devaluation of USD. [6] Looking into details, the import price climbed upward before 2005, which was due to the rapid growing crude oil price during that time. This in some ways lead to the LNG import decrease in 2005 and 2006 (Fig. 1). A turning point of the price curve occurred in 2006, when it dropped by about 15% and kept at low level for 2007. This partially explains the increases in natural gas imports in 2007 shown in Fig. 1. At 2008, LNG import price climbed to the same peak as happened before the year of 2006 and then dropped sharply, which was in same trend with oil price. As to the US LNG export price, it keeps on a upward trend even after 2008 when the oil price dropped significantly. This rise is probably due to the growing demand for LNG in the Asian countries including Thailand, China, Japan and India, which is said to be 13% year-over-year by Barclays' analysis. [7]

|

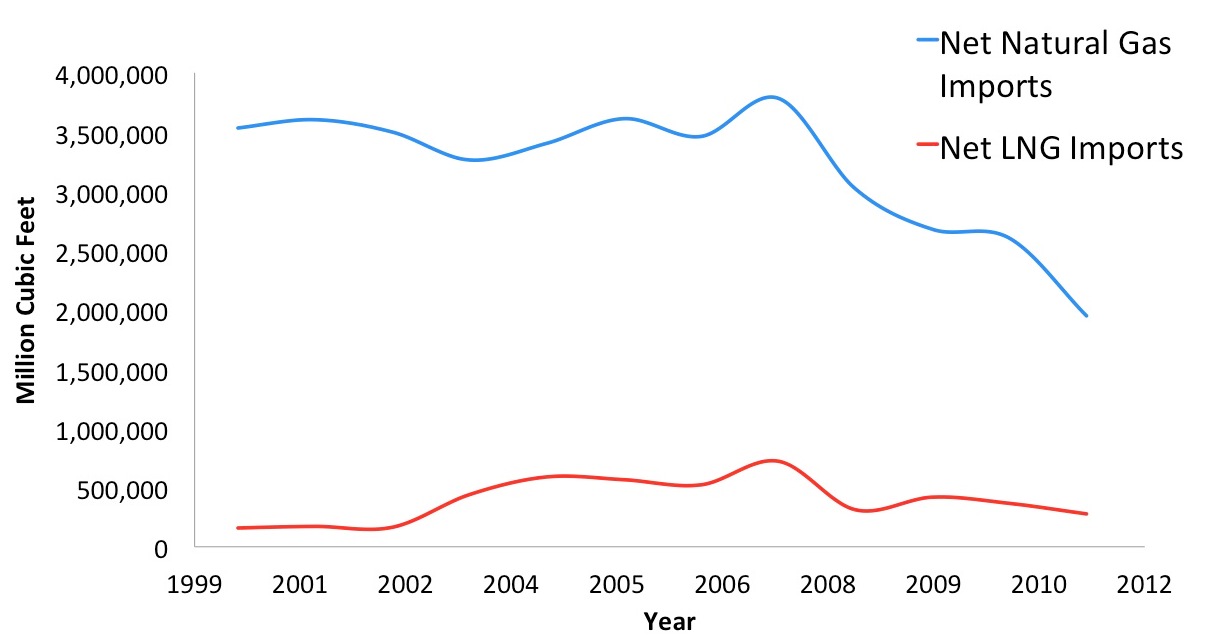

| Fig. 3: Net US Natural Gas Imports. [2-5] |

Another important message from Fig. 2 is that the gas price in domestic market is considerably lower than export price for LNG (5 dollars per thousand cubic feet compared to over 10 dollars per thousand cubic feet). Such a large price gap will spur the US gas companies to expand their oversea LNG business and reorientation of the LNG market towards Asia will occur.

Combing the US Natural Gas Imports and Exports, it is predicted that the US will be less and less dependent of gas importing (Fig. 3). If doing linear extrapolation, it is expected that US will no longer need to import gas before 2020 and then start net exporting of gas. This significant transformation should mainly attribute to the development of shale gas in the US. That it so say, the US will turn from a heavy gas imports dependent country to a gas exporting country in the near future if the gas price stays at an appropriate level.

© Yisha Mao. The author grants permission to copy, distribute and display this work in unaltered form, with attribution to the author, for noncommercial purposes only. All other rights, including commercial rights, are reserved to the author.

[1] S. Kumar et al., "Current Status and Future Projections of LNG Demand and Supplies: Global Prospective," Energy Policy 39, 4097 (2011).

[2] "Natural Gas Annual 1996," U.S. Energy Information Administration, DOE/EIA-0131(96), September 1997.

[3] "Natural Gas Annual 2001," U.S. Energy Information Administration, DOE/EIA-0131(01), February 2003.

[4] "Natural Gas Annual 2006," U.S. Energy Information Administration, DOE/EIA-0131(06), October 2007.

[5] "Natural Gas Annual 2010," U.S. Energy Information Administration, DOE/EIA-0131(10), December 2011.

[6] "The Global Liquefied Natural Gas Market: Status & Outlook," U.S. Energy Information Administration, DOE/EIA-0637 (2003), December 2003.

[7] "Barclays: LNG Seeing Very Slow Growth So Far in 2012," Oil and Gas Journal, 15 Oct 12.